#Computer Engineering Market Demand 2023

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

28.6 is the average number of monthly visits per US mobile user.

Text

#Computer Engineering Industry Analysis 2023#Computer Engineering Industry Analysis 2022#Computer Engineering Market 2023#Computer Engineering Market Analysis#Computer Engineering Market Data#Computer Engineering Market Demand 2023#Computer Engineering market forecast 2023#Computer Engineering Market Growth#Computer Engineering Market In Apac#Computer Engineering Market in Europe#Computer Engineering market in US 2023#Computer Engineering Market Outlook 2023#Computer Engineering Market players#Computer Engineering Market in United States#Computer Engineering Market in Spain#Computer Engineering Market in Germany#Computer Engineering Market in Saudi Arabia#Computer Engineering Market Singapore#Computer Engineering Market in Australia#Computer Engineering Market in United Kingdom

0 notes

Text

2025 Predictions: Disruption, M&A, and Cultural Shifts

1. NVIDIA’s Stock Faces a Correction

After years of market dominance driven by AI and compute demand, investor expectations will become unsustainable. A modest setback—whether technical, regulatory, or competitive—will trigger a wave of profit-taking and portfolio rebalancing among institutional investors, ending the year with NVIDIA’s stock below its January 2025 price.

2. OpenAI Launches a Consumer Suite to Rival Google

OpenAI will aggressively debut “Omail,” “Omaps,” and other consumer products, subsidizing adoption with cash incentives (e.g., $50/year for Omail users). The goal: capture original user-generated data to train models while undercutting Google’s monetization playbook. Gen Z, indifferent to legacy tech brands, will flock to OpenAI’s clean, ad-light alternatives.

3. Rivian Gains Momentum as Tesla’s Talent Exodus Begins

Despite fading EV subsidies, Rivian becomes a credible challenger as Tesla grapples with defections. Senior Tesla executives—disillusioned with Elon Musk’s polarizing brand—will migrate to Rivian, accelerating its R&D and operational maturity. By late 2025, Rivian’s roadmap hints at long-term disruption, though Tesla’s scale remains unmatched.

4. Ethereum and Vitalik Surge to New Heights

Ethereum solidifies its role as crypto’s foundational layer, driven by institutional DeFi adoption and regulatory clarity. Vitalik Buterin transcends “crypto-founder” status, becoming a global thought leader on digital governance and AI ethics. His influence cements ETH’s position as the “defacto choice” of decentralized ecosystems.

5. Amazon Acquires Anthropic in a $30B AI Play

Amazon, needing cutting-edge AI to compete with Microsoft/OpenAI and Google, buys Anthropic but preserves its independence (a la Zappos). Anthropic’s “long-term governance” model becomes a differentiator, enabling multi-decade AI safety research while feeding Amazon’s commercial ambitions.

6. Netflix Buys Scopely to Dominate Interactive Entertainment

With streaming growth plateauing, Netflix doubles down on gaming. The $10B Scopely acquisition adds hit mobile titles (Star Trek Fleet Command, Marvel Strike Force) to its portfolio, creating a subscription gaming bundle that meshes with its IP-driven content engine.

7. Amazon + Equinox + Whole Foods = Wellness Ecosystems

Amazon merges Equinox’s luxury fitness brand with Whole Foods’ footprint, launching “Whole Life” hubs: members work out, sauna, grab chef-prepared meals at the hot bar, and shop for groceries—all under one subscription.

8. Professional Sports Become the Ultimate Cultural Currency

Athletes supplant Hollywood stars as cultural icons, with leagues monetizing 24/7 fandom via microtransactions (NFT highlights, AI-personalized broadcasts). Even as streaming fragments TV rights, live sports’ monopoly on real-time attention fuels record valuations.

9. Bryan Johnson’s Blueprint Goes Mainstream

Dismissed as a biohacking meme in 2023, Blueprint pivots from $1,000/month “vampire face cream” to a science-backed longevity brand. Partnering with retail giants, it dominates the $50B supplement market and other longevity products (hair loss, ED, etc).

10. Jayden Daniels Redefines QB Training with Neurotech

The Commanders’ rookie stuns the NFL with pre-snap precision honed via AR/VR simulations that accelerate cognitive processing. His startup JaydenVision, licenses the tech to the league—making “brain reps” as routine as weightlifting by 2026.

*BONUS*

11. YouTube Spins Out, Dwarfing Google’s Valuation

Alphabet spins off YouTube into a standalone public company. Unleashed from Google’s baggage, YouTube capitalizes on its creator economy, shoppable videos, and AI-driven content tools. Its market cap surpasses $1.5T—eclipsing Google’s core search business.

3 notes

·

View notes

Text

CNC development history and processing principles

CNC machine tools are also called Computerized Numerical Control (CNC for short). They are mechatronics products that use digital information to control machine tools. They record the relative position between the tool and the workpiece, the start and stop of the machine tool, the spindle speed change, the workpiece loosening and clamping, the tool selection, the start and stop of the cooling pump and other operations and sequence actions on the control medium with digital codes, and then send the digital information to the CNC device or computer, which will decode and calculate, issue instructions to control the machine tool servo system or other actuators, so that the machine tool can process the required workpiece.

1. The evolution of CNC technology: from mechanical gears to digital codes

The Beginning of Mechanical Control (late 19th century - 1940s)

The prototype of CNC technology can be traced back to the invention of mechanical automatic machine tools in the 19th century. In 1887, the cam-controlled lathe invented by American engineer Herman realized "programmed" processing for the first time by rotating cams to drive tool movement. Although this mechanical programming method is inefficient, it provides a key idea for subsequent CNC technology. During World War II, the surge in demand for military equipment accelerated the innovation of processing technology, but the processing capacity of traditional machine tools for complex parts had reached a bottleneck.

The electronic revolution (1950s-1970s)

After World War II, manufacturing industries mostly relied on manual operations. After workers understood the drawings, they manually operated machine tools to process parts. This way of producing products was costly, inefficient, and the quality was not guaranteed. In 1952, John Parsons' team at the Massachusetts Institute of Technology (MIT) developed the world's first CNC milling machine, which input instructions through punched paper tape, marking the official birth of CNC technology. The core breakthrough of this stage was "digital signals replacing mechanical transmission" - servo motors replaced gears and connecting rods, and code instructions replaced manual adjustments. In the 1960s, the popularity of integrated circuits reduced the size and cost of CNC systems. Japanese companies such as Fanuc launched commercial CNC equipment, and the automotive and aviation industries took the lead in introducing CNC production lines.

Integration of computer technology (1980s-2000s)

With the maturity of microprocessor and graphical interface technology, CNC entered the PC control era. In 1982, Siemens of Germany launched the first microprocessor-based CNC system Sinumerik 800, whose programming efficiency was 100 times higher than that of paper tape. The integration of CAD (computer-aided design) and CAM (computer-aided manufacturing) software allows engineers to directly convert 3D models into machining codes, and the machining accuracy of complex surfaces reaches the micron level. During this period, equipment such as five-axis linkage machining centers came into being, promoting the rapid development of mold manufacturing and medical device industries.

Intelligence and networking (21st century to present)

The Internet of Things and artificial intelligence technologies have given CNC machine tools new vitality. Modern CNC systems use sensors to monitor parameters such as cutting force and temperature in real time, and use machine learning to optimize processing paths. For example, the iSMART Factory solution of Japan's Mazak Company achieves intelligent scheduling of hundreds of machine tools through cloud collaboration. In 2023, the global CNC machine tool market size has exceeded US$80 billion, and China has become the largest manufacturing country with a production share of 31%.

2. CNC machining principles: How code drives steel

The essence of CNC technology is to convert the physical machining process into a control closed loop of digital signals. Its operation logic can be divided into three stages:

Geometric Modeling and Programming

After building a 3D model using CAD software such as UG and SolidWorks, CAM software “deconstructs” the model: automatically calculating parameters such as tool path, feed rate, spindle speed, and generating G code (such as G01 X100 Y200 F500 for linear interpolation to coordinates (100,200) and feed rate 500mm/min). Modern software can even simulate the material removal process and predict machining errors.

Numerical control system analysis and implementation

The "brain" of CNC machine tools - the numerical control system (such as Fanuc 30i, Siemens 840D) converts G codes into electrical pulse signals. Taking a three-axis milling machine as an example, the servo motors of the X/Y/Z axes receive pulse commands and convert rotary motion into linear displacement through ball screws, with a positioning accuracy of up to ±0.002mm. The closed-loop control system uses a grating ruler to feedback position errors in real time, forming a dynamic correction mechanism.

Multi-physics collaborative control

During the machining process, the machine tool needs to coordinate multiple parameters synchronously: the spindle motor drives the tool to rotate at a high speed of 20,000 rpm, the cooling system sprays atomized cutting fluid to reduce the temperature, and the tool changing robot completes the tool change within 0.5 seconds. For example, when machining titanium alloy blades, the system needs to dynamically adjust the cutting depth according to the hardness of the material to avoid tool chipping.

3. The future of CNC technology: cross-dimensional breakthroughs and industrial transformation

Currently, CNC technology is facing three major trends:

Combined: Turning and milling machine tools can complete turning, milling, grinding and other processes on one device, reducing clamping time by 90%;

Additive-subtractive integration: Germany's DMG MORI's LASERTEC series machine tools combine 3D printing and CNC finishing to directly manufacture aerospace engine combustion chambers;

Digital Twin: By using a virtual machine tool to simulate the actual machining process, China's Shenyang Machine Tool's i5 system has increased debugging efficiency by 70%.

From the meshing of mechanical gears to the flow of digital signals, CNC technology has rewritten the underlying logic of the manufacturing industry in 70 years. It is not only an upgrade of machine tools, but also a leap in the ability of humans to transform abstract thinking into physical entities. In the new track of intelligent manufacturing, CNC technology will continue to break through the limits of materials, precision and efficiency, and write a new chapter for industrial civilization.

#prototype machining#cnc machining#precision machining#prototyping#rapid prototyping#machining parts

2 notes

·

View notes

Text

US Tech Stocks Stabilize After DeepSeek AI App Disrupts Market

US Tech Stocks Stabilize After DeepSeek AI App Disrupts Market

US tech stocks held steady on Tuesday after experiencing a sharp decline on Monday, triggered by the unexpected rise of the Chinese-made artificial intelligence (AI) app, DeepSeek.

Shares of chip giant Nvidia, which had fallen sharply on Monday, rebounded by 8.8% as experts suggested the AI market selloff may have been an overreaction. Investors were quick to adjust their positions after DeepSeek claimed its AI model was developed at a fraction of the cost of its competitors' offerings.

The news sparked concerns over the future of America's AI dominance and raised questions about the scale of investments US companies are planning. US President Donald Trump described the situation as "a wake-up call" for the tech industry, while also suggesting that the development could ultimately be beneficial for the US economy. He remarked that if AI models could be produced more cheaply while delivering the same results, it would be a positive outcome for the country.

Trump downplayed concerns, emphasizing that the US would remain a key player in the AI field. The surge of optimism around AI investments has fueled much of the US stock market's growth over the past two years, prompting fears of a potential market bubble.

DeepSeek, launched just a week ago, quickly became the most downloaded free app in the US. Its rise comes amid ongoing tensions between the US and China over AI technology, with the US restricting the export of advanced AI chips to China.

Chinese AI developers, facing limited access to these chips, have shared research and explored alternative approaches that demand less computational power. This has led to the creation of AI models that are significantly cheaper to produce, challenging industry norms and threatening to disrupt the market.

Nvidia, the leading provider of advanced chips used in many AI applications, was hit hardest by the market selloff. Its share price dropped 17% on Monday, erasing nearly $600 billion from its market value.

Analysts, including Janet Mui of RBC Brewin Dolphin, explained that investors typically respond with caution to groundbreaking developments due to uncertainty. However, she noted that the cheaper AI models could benefit tech giants such as Apple and other firms, who have faced scrutiny over their high AI investments.

After the initial shock, US stock markets stabilized on Tuesday. The Dow Jones Industrial Average rose 0.3%, the S&P 500 gained nearly 1%, and the Nasdaq saw a 2% increase. In the UK, the FTSE 100 closed 0.35% higher. Meanwhile, AI-related stocks in Japan, including Advantest, SoftBank, and Tokyo Electron, saw sharp declines, contributing to a 1.4% drop in the Nikkei 225. Several Asian markets remained closed for the Lunar New Year holiday, with mainland China's markets set to reopen on February 5.

DeepSeek's Founder: Liang Wenfeng

DeepSeek was founded in 2023 by Liang Wenfeng in Hangzhou, China. The 40-year-old, an engineering graduate, also established the hedge fund that financed the development of the AI app. Liang recently attended a meeting with industry leaders and Chinese Premier Li Qiang. In a July 2024 interview, he expressed surprise at the sensitivity surrounding the pricing of his AI models, stating that the company had simply focused on cost-efficient development and pricing without anticipating such a reaction from the market.

3 notes

·

View notes

Text

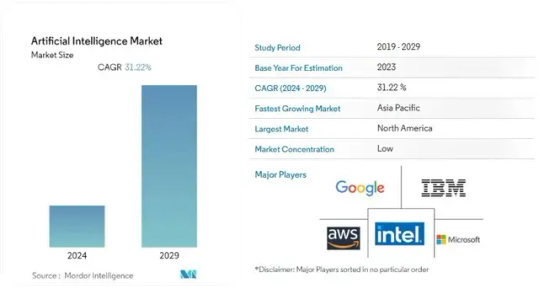

Embrace the Future with AI 🚀

The AI industry is set to skyrocket from USD 2.41 trillion in 2023 to a projected USD 30.13 trillion by 2032, growing at a phenomenal CAGR of 32.4%! The AI market continues to experience robust growth driven by advancements in machine learning, natural language processing, and cloud computing. Key industry player heavily invests in AI to enhance their product offerings and gain competitive advantages.

Here is a brief analysis of why and how AI can transform businesses to stay ahead in the digital age.

Key Trends:

Predictive Analytics: There’s an increasing demand for predictive analytics solutions across various industries to leverage data-driven decision-making.

Data Generation: Massive growth in data generation due to technological advancements is pushing the demand for AI solutions.

Cloud Adoption: The adoption of cloud-based applications and services is accelerating AI implementation.

Consumer Experience: Companies are focusing on enhancing consumer experience through AI-driven personalized services.

Challenges:

Initial Costs: High initial costs and concerns over replacing the human workforce.

Skill Gap: A lack of skilled AI technicians and experts.

Data Privacy: Concerns regarding data privacy and security.

Vabro is excited to announce the launch of Vabro Genie, one of the most intelligent SaaS AI engines. Vabro Genie helps companies manage projects, DevOps, and workflows with unprecedented efficiency and intelligence. Don’t miss out on leveraging this game-changing tool!

Visit www.vabro.com

#ArtificialIntelligence#TechTrends#Innovation#Vabro#AI#VabroGenie#ProjectManagement#DevOps#Workflows#Scrum#Agile

3 notes

·

View notes

Text

Drilling Data Management Systems Market Navigates a New Era of Predictive Exploration

The Drilling data management systems market was valued at USD 3.7 billion in 2023 and is expected to reach USD 12.7 billion by 2032, growing at a CAGR of 14.79% from 2024-2032.

Drilling Data Management Systems Market is witnessing significant transformation as energy companies aim to optimize operational efficiency and make data-driven decisions. With the increasing complexity of drilling activities and demand for precision, these systems are becoming essential for tracking real-time performance, reducing downtime, and managing costs effectively.

U.S. Market Sees Rapid Adoption of Real-Time Data Solutions for Drilling Efficiency

Drilling Data Management Systems Market continues to evolve with the integration of cloud computing, IoT, and advanced analytics. As the industry shifts towards digital oilfields, organizations are investing in scalable and intelligent solutions that ensure safe, efficient, and environmentally compliant drilling operations.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6647

Market Keyplayers:

Schlumberger – Petrel E&P Software Platform

Halliburton – DecisionSpace Well Engineering

Baker Hughes – JewelSuite Subsurface Modeling

Emerson – Paradigm Geolog

Kongsberg Digital – SiteCom

Pason Systems – DataHub

Weatherford – Centro Digital Well Delivery

CGG – GeoSoftware

PetroVue – PetroVue Analytics Platform

Katalyst Data Management – iGlass

Peloton – WellView

IDS – DrillNet

DataCloud – MinePortal

TDE Group – tde proNova

NOV – NOVOS

Market Analysis

The Drilling Data Management Systems Market is gaining traction due to the growing need for accurate data integration, performance monitoring, and regulatory compliance. As drilling operations become more data-intensive, the ability to consolidate and analyze vast volumes of data in real time is critical. North America, particularly the U.S., leads in adoption due to its extensive oil & gas activities and early implementation of digital infrastructure. Meanwhile, Europe is investing in sustainable drilling technologies, boosting the demand for data management platforms that support environmental goals.

Market Trends

Growing integration of AI and machine learning for predictive analytics

Rise in cloud-based platforms offering scalable and remote accessibility

Increased demand for real-time drilling data visualization

Expansion of edge computing for on-site data processing

Enhanced cybersecurity features to protect sensitive operational data

Adoption of mobile dashboards and automated reporting tools

Demand for interoperability between legacy systems and new platforms

Market Scope

The scope of the drilling data management systems market extends across upstream oil & gas sectors, where efficient data collection and analysis are pivotal. As energy exploration enters more challenging environments, these systems offer a critical edge.

Real-time data acquisition from drilling sites

Integration with IoT-enabled sensors and control systems

Predictive maintenance powered by historical data

Customizable dashboards and alert systems

Advanced compliance reporting to meet regulatory standards

Seamless collaboration across global drilling teams

Forecast Outlook

The future of the Drilling Data Management Systems Market looks promising as energy companies move towards full-scale digitization of operations. The increasing focus on sustainability, safety, and efficiency is expected to drive innovation in data management technologies. Adoption will be further propelled by the need to reduce costs, improve well integrity, and make smarter, faster drilling decisions. Both U.S. and European markets will remain instrumental in shaping this evolution through continuous investments in tech-driven exploration strategies.

Access Complete Report: https://www.snsinsider.com/reports/drilling-data-management-systems-market-6647

Conclusion

As the global energy sector navigates a digital revolution, drilling data management systems have emerged as a cornerstone of modern oilfield operations. From the shale basins of Texas to the offshore rigs of the North Sea, these platforms empower organizations to transform raw data into actionable insights. With rising complexity and expectations, embracing intelligent data systems isn’t just a trend—it’s a competitive imperative for a safer, smarter, and more profitable drilling future.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Related Reports:

U.S.A embraces cutting-edge AI innovation with rising adoption in Synthetic Data Generation Market

U.S.A embraces Performance Marketing Software for data-driven campaign optimization

U.S.A enterprises prioritize robust data governance with Enterprise Metadata Management (EMM) adoption on the rise

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

#Drilling Data Management Systems Market#Drilling Data Management Systems Market Scope#Drilling Data Management Systems Market Growth

0 notes

Text

Thin Client Market Leaders: Top Companies to Watch in 2025

The global thin client market, valued at USD 1.60 billion in 2023, is projected to reach USD 1.97 billion by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 3.0% from 2024 to 2030. This expansion is largely driven by the increasing need for new revenue engines and efficient business growth strategies. As modern applications become more diverse in technologies and platforms, businesses face challenges in data integration and compliance, leading to reduced data visibility and hindered decision-making.

The COVID-19 pandemic positively impacted this market, reshaping dynamics and accelerating adoption. Pandemic-induced economic uncertainties pushed organizations towards cost-effective IT solutions. Thin clients, with their lower upfront costs compared to traditional PCs and laptops, coupled with centralized management capabilities that reduce ongoing maintenance and support expenses, proved to be an attractive option.

Key Market Trends & Insights:

Regional Dominance: North America dominated the thin client market in 2023, holding a 35.7% market share. This is primarily due to the rising adoption of Remote Desktop Services (RDS) and Desktop as a Service (DaaS) models in the region.

Component Leadership: Based on type, the market is bifurcated into hardware, software, and services. The hardware segment accounted for the largest revenue share, 38.4% in 2023, and is expected to maintain its dominance throughout the forecast period.

Form Factor Preference: The market, segmented by form factor into standalone, with monitor, and mobile, saw the mobile segment hold the largest revenue share in 2023. This segment is also anticipated to experience the fastest CAGR during the forecast period, indicating a growing demand for portable thin client solutions.

Application Focus: The market is further bifurcated by application into healthcare, retail, education, government, and others. The education segment accounted for the largest revenue share in 2023, reflecting the significant adoption of thin client technology in educational institutions.

Order a free sample PDF of the Thin Client Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2023 Market Size: USD 1.60 Billion

2030 Projected Market Size: USD 1.97 Billion

CAGR (2024 - 2030): 3.0%

North America: Largest market in 2023

Key Companies & Market Share Insights

Accenture, IBM, and Infosys are prominent players in the thin client market, each leveraging their expertise to drive digital transformation.

Accenture focuses on enabling digital transformation through thin client solutions, emphasizing a microservices architecture and containerization for agility and efficient resource utilization. Their approach integrates DevOps practices for faster development and collaboration. Security and data modernization strategies are central to their offerings, enhancing analytics and compliance. Accenture also specializes in seamless legacy system integration, providing a strategic path for organizations to reduce technical debt and ensure sustained success in a dynamic digital landscape.

IBM promotes a DevOps culture to foster collaboration and efficiency in software development. Their services incorporate rigorous security measures to protect applications and data. With a strong commitment to user experience, IBM's modernization services deliver revamped interfaces and intuitive interactions. By integrating analytics and data modernization strategies, IBM empowers organizations to navigate complex modern digital environments while optimizing the integration of existing legacy systems.

Infosys Limited, a global consulting and technology company, offers extensive expertise in thin client technology within its diverse service portfolio. This computing model centralizes application processing and data storage on a server, allowing client devices to access these resources remotely over a network. Furthermore, Infosys provides comprehensive ongoing support and maintenance services to ensure the smooth operation and continuous optimization of thin client environments for its clients.

Key Players

IBM

Accenture

Infosys

Cognizant

Capgemini

Tata Consultancy Services

DXC Technology

HCL Technologies

Wipro

NTT DATA Corporation

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The thin client market is expanding, driven by the need for efficient business growth and challenges in data integration. The pandemic also accelerated adoption due to the demand for cost-effective IT solutions. North America leads the market, with hardware dominating component types, and mobile thin clients showing the fastest growth. The education sector is a major application area. Key players like Accenture, IBM, and Infosys are innovating in digital transformation, security, and integration to meet evolving market demands.

0 notes

Text

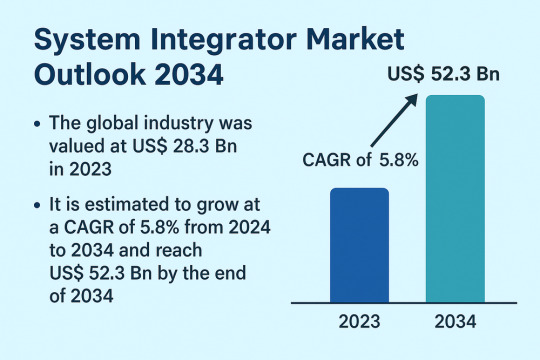

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

2D vs 3D Animation: Key Differences Every Learner Should Know

The world of animation has expanded beyond the bounds of traditional storytelling. From social media reels to Netflix originals and from mobile games to blockbuster films, animation is everywhere. But if you're just stepping into this vibrant domain, one of the first dilemmas you’ll face is choosing between 2D and 3D animation. They are both incredibly powerful, yet vastly different in style, technique, and application. So, what exactly sets them apart, and which one is right for you?

Let’s break it down.

Understanding 2D Animation

2D animation refers to characters and environments created in a two-dimensional space. Think classic Disney films like The Lion King or TV shows like Rick and Morty. The movement is drawn frame-by-frame, often using digital tools today (rather than pencil and paper).

Core features of 2D animation:

Flat visual style: Focuses on height and width but lacks depth.

Frame-by-frame drawing: Each movement is created through individual frames, which can be labor-intensive.

Tools used: Adobe Animate, Toon Boom Harmony, and TVPaint are popular software choices.

Advantages:

Simpler and faster to produce (depending on complexity).

Easier to master for beginners.

Stylized and visually expressive—ideal for storytelling, explainer videos, and mobile games.

Challenges:

Less realistic when compared to 3D.

Requires strong illustration skills.

Limited in simulating complex motion or camera angles.

Understanding 3D Animation

3D animation brings characters and objects to life in a three-dimensional space, giving them depth and realism. This is the style used in films like Toy Story, video games like Assassin’s Creed, and architectural walkthroughs.

Core features of 3D animation:

Real-world physics: Lighting, shadows, textures, and camera angles mimic real environments.

Rigging and modeling: Instead of drawing each frame, animators create a digital model (character), rig it with a skeleton, and move it like a puppet.

Software tools: Autodesk Maya, Blender, Cinema 4D, and Houdini are industry standards.

Advantages:

Highly realistic and immersive.

Ideal for high-budget films, gaming, VR/AR, and simulations.

Once a model is rigged, it’s reusable—reducing effort on repetitive motion.

Challenges:

Steep learning curve.

Demands more computing power.

Often requires teamwork across modeling, texturing, lighting, and animating roles.

Market Demand: 2D vs. 3D

From a career standpoint, the choice between 2D and 3D often depends on your goals and the industry you’re eyeing. While 2D is still widely used in mobile apps, social media content, and educational videos, 3D dominates in film, gaming, and emerging fields like virtual production.

According to Statista, the global animation market was valued at over $370 billion in 2023, with 3D animation accounting for a significant portion of that growth. Even within advertising and product design, brands are increasingly leaning towards 3D to create more dynamic and engaging experiences.

That said, platforms like YouTube and Instagram continue to thrive on 2D storytelling due to its faster production cycle and relatable aesthetic. Shows like BoJack Horseman and Adventure Time prove that 2D isn’t going away—it’s just evolving with digital tools.

Skillsets and Career Paths

If you choose 2D animation, you may become:

Character animator

Storyboard artist

Motion graphics designer

Background artist

Comic illustrator

If you choose 3D animation, you could specialize in:

3D modeler

Character rigger

VFX artist

Environment designer

Technical animator

Both fields offer freelance and full-time opportunities. Moreover, hybrid skills—like combining 2D and 3D for stylized visuals (as seen in Spider-Man: Into the Spider-Verse)—are increasingly valued in the industry.

Latest Trends and News

Animation is undergoing a shift thanks to real-time engines like Unreal Engine and Unity, which allow animators to produce stunning visuals with shorter turnaround times. This is especially revolutionizing 3D animation and game design workflows. MetaHuman Creator by Epic Games is enabling hyper-realistic 3D characters with pre-built rigs, reducing production bottlenecks.

Meanwhile, 2D animation has been given new life by AI-assisted tools like Adobe’s Project Blink and Runway ML, which automate certain parts of frame transitions and coloring. This allows smaller teams to create high-quality 2D content faster and more affordably.

Another emerging trend is 2.5D animation, where 2D characters interact in a simulated 3D environment—offering a balance between both worlds.

Which One Should You Learn?

Now for the big question: 2D or 3D?

Ask yourself:

What kind of stories do you want to tell? If you're into whimsical, stylized storytelling or short-form content, 2D might be your space.

Are you tech-savvy and curious about physics and realism? 3D offers more technical depth and opens doors to industries like gaming, AR/VR, and film.

What's your learning timeline and equipment availability? 2D can be started with minimal gear and simpler software, whereas 3D may require more robust tools and system configurations.

Do you want to specialize or become a generalist? If you're looking to freelance across media types, 2D might be more adaptable. For those wanting to work on AAA games or VFX-heavy films, 3D is essential.

Ultimately, you don’t need to choose forever. Many animators today are hybrid professionals—starting in one and eventually learning both as their career evolves. The foundational skills of animation—timing, movement, storytelling—are universal.

A Note on Industry Growth

Cities across India are rapidly developing as animation hubs, and Bengaluru stands out with its increasing demand for both 2D and 3D professionals. With production houses, ad agencies, gaming studios, and edtech companies expanding their in-house creative teams, the interest in formal learning has surged. Whether it’s traditional techniques or cutting-edge software, taking an Animation course in Bengaluru can open doors to diverse career paths in an increasingly competitive market.

Conclusion

In the end, the “better” choice between 2D and 3D animation isn't universal—it’s personal. It comes down to what excites you, where you see your strengths, and the kind of visual world you want to create. Both styles have their charm, technical depth, and career potential. So, instead of asking which is superior, ask which one aligns with your creative goals right now.

As India’s animation industry grows, Bengaluru continues to evolve into a hub for innovation and talent. Whether you aim to be part of a game design studio or a creative tech company, enrolling in a 3D animation course bengaluru could be the first step toward building an exciting future in this dynamic field.

0 notes

Text

Tech Ready: Why Data Centers Are Turning to Pre-Engineered Buildings

The sharp rise in data usage and the rapid growth of the digital economy are fueling demand for larger, more advanced data centers. But the question is: Can your tech business build fast enough to keep up? If you move away from traditional construction methods, you can use pre-engineered metal buildings (PEMBs) instead. These structures offer a faster, lower-risk way to get critical infrastructure up and running, with streamlined on-site assembly and shorter build times.

At Armstrong Steel, we understand the urgency behind scaling infrastructure for cloud computing, secure server storage, and other tech applications. Let’s break down how pre-engineered metal buildings meet the unique demands of data center construction — from speed and flexibility to cost control and energy performance.

The rise of data centers and how PEMBs help

Data centers are the cornerstone of today’s digital economy. Every cloud computing, streaming, and click depends on these facilities, so it’s no surprise that the global data center market is set to grow at a CAGR of 12.5% from 2023 to 2030. But meeting that demand isn't easy — tech companies are under pressure to build smarter, faster, and more adaptable infrastructure. Here’s what they’re up against:

Scalability: Data centers must grow or adapt as quickly as digital needs evolve. Facilities should allow for seamless expansion or downsizing — whether that means adding more server space or reconfiguring layouts — without major cost or construction disruptions.

Energy efficiency: Running a data center requires a massive and constant supply of electricity. Businesses must find ways to optimize energy use through better insulation, cooling systems, and layout planning, all while maintaining performance and keeping operational costs under control.

Aesthetic appeal: In modern business parks or tech campuses, functionality alone isn’t enough. Data centers are part of a company’s brand image, so the exterior design should reflect professionalism and architectural quality.

Speed of expansion: With market demands shifting fast, data centers must be built and expanded quickly. Long construction timelines can mean missed opportunities, so companies need building solutions that speed up delivery without compromising on quality or safety.

The answer: PEMBs

Pre-engineered metal buildings address these challenges with the speed, energy efficiency, and flexibility they offer. Unlike traditional construction, these structures are ready to assemble and erect on site. With PEMBs, you can build a functional and aesthetically pleasing data center quickly and cost-effectively.

The benefits of pre-engineered steel data center buildings

Traditional construction using wood, concrete, and masonry will only delay your project. Meanwhile, pre-engineered metal buildings can keep pace with the flexibility and speed expected in data center construction. Here’s a more in-depth look at the benefits of PEMBs and why they make excellent data centers.

Speedy construction

One of the significant benefits of PEMBs is their quick construction. We make all components of your prefabricated steel building kit in our factory under controlled conditions, ensuring each aspect is carefully engineered to your local building codes, loads, and environmental conditions. This approach could reduce the project timeline by up to 50%.

If you need a data center within 6 months, choosing pre-engineered metal buildingswill allow you to meet that deadline without compromising quality and structural integrity. At Armstrong Steel, we make prefab steel buildings with custom assembly drawings, anchor bolt patterns, and a comprehensive erection guide. The major connections are already punched and ready to bolt together. Moreover, most components are cut and numbered, so you can assemble them based on the drawings.

Flexible designs

Pre-engineered metal buildings are highly customizable. At Armstrong Steel, we can customize the prefab steel building kit to meet your data center’s unique dimensions, layout, and structural needs. Their modular layouts allow endless expansions in the future. In addition, our designs can accommodate any external or internal finish or wall and roofing option, ensuring your building won't look too industrial.

Whether you require a modular or clear-span structure, we can accommodate any design requirement. This flexibility allows you to make the most of the space. For instance, you can incorporate a mix of modular community spaces, offices, an open-plan workspace, and a spacious server room that can adapt to your growing requirements.

Cost-effectiveness

Pre-engineered metal buildings are quick to assemble and erect, contributing to reduced labor costs. Each part is pre-fabricated, reducing material waste and surprise costs. Plus, their low maintenance needs and durability bring long-term savings.

Durable, worry-free data centers

You won’t have to worry about extreme weather when you use a pre-engineered metal building for your data center. These structures are strong and can withstand high winds, hurricanes, and heavy snowfall. Plus, we engineer them to withstand the seismic activity in your region. Building with steel also protects your data center against fires. It’s non-combustible, so it’s unlikely for fire to spread too quickly and burn everything down.

Energy efficiency

Today’s pre-engineered metal buildings are more energy efficient, thanks to modern insulation technologies. They are easy to integrate with solar-ready roofing, insulated metal panels, and sophisticated ventilation systems. These features can help reduce your energy costs, saving you money down the road.

Let’s design a high-quality data center for your business.

Get in touch with our team here at Armstrong Steel if you’re interested in pre-engineered metal buildings for your data center. We’ll work with you to design and manufacture the perfect structure that meets your exact requirements. Additionally, we will make sure your building is delivered on time. Call us at 1-800-345-4610 to get started now, or click ‘Price My Building’ to get a custom quote.

0 notes

Text

Comprehensive Study of the Global Space Robotics Industry

The global space robotics market was valued at USD 4.40 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 8.8% from 2023 to 2030. This robust growth trajectory is driven by the increasing need for efficient repair, servicing, and maintenance of geostationary satellites, as well as the cost-efficiency and superior operational performance of robotic systems in the extreme conditions of space.

The growing demand for autonomous systems and robotics technologies is being further fueled by the accelerating number of space missions worldwide. The success of advanced space programs such as on-orbit satellite servicing, manufacturing, and assembly operations aboard the International Space Station (ISS)—as well as the Lunar Surface Innovation Initiative by NASA—requires sophisticated robotics capable of executing complex tasks with precision and reliability.

Leading space agencies are investing in strategic roadmaps to guide the future of space robotics. For example, NASA's space technology roadmap to 2035 prioritizes several key robotic capabilities. Similarly, the European Space Agency (ESA) supports space robotics innovation through European Commission–funded initiatives such as PERASPERA and SpacePlan 2020. PERASPERA, in particular, is developing a cohesive master plan for European space robotics for implementation during 2023–2024. Beyond the U.S. and Europe, nations including China, Russia, India, and Japan are expanding their space programs and increasingly incorporating robotics into mission-critical roles.

Space robots, designed as mission-defined autonomous machines, can conduct a wide range of operations including planetary exploration, satellite servicing, assembly, and maintenance tasks. These robotic systems are vital for extending human reach in space, supporting astronauts, and executing remote operations with minimal human intervention. Their development represents a convergence of mechanical engineering, computer science, artificial intelligence, and space sciences, significantly broadening their range of applications across both manned and unmanned missions.

Emerging technologies, notably Artificial Intelligence (AI) and Deep Learning (DL), are revolutionizing space robotics by enabling smarter, more adaptive robotic systems. These advancements allow for enhanced autonomy, improved mobility, and more efficient data processing in harsh space environments. A recent example of innovation in this area is the Int-Ball, an autonomous internal camera developed by the Japan Aerospace Exploration Agency (JAXA). Deployed aboard the ISS in June 2023, Int-Ball autonomously navigates to specific positions to capture photos and videos, thereby reducing the workload on astronauts and streamlining onboard documentation processes. Controlled remotely by JAXA's ground teams, the Int-Ball reflects the increasing reliance on AI-driven robotics in space operations.

Another key market driver is the rapid increase in satellite launches, which has created a surge in demand for on-orbit servicing, debris removal, and robotic assembly. The congestion of Earth’s orbit due to satellite proliferation poses a significant threat to current and future missions. This has intensified the focus on developing dexterous robotic manipulators capable of capturing, repairing, maintaining, and de-orbiting dysfunctional or aging satellites. Technologies like In-Space Robotic Assembly (ISRA) and Extra-Vehicular Activity (EVA) robotics are becoming essential tools in mitigating orbital debris and supporting long-term space sustainability.

As the commercial and governmental space sectors continue to expand, the need for advanced space robotics solutions will become even more critical. The integration of AI, machine vision, autonomous navigation, and advanced materials into robotic platforms will pave the way for a new era in space exploration, colonization, and infrastructure development.

Get a preview of the latest developments in the Space Robotics Market? Download your FREE sample PDF copy today and explore key data and trends

Detailed Segmentation:

The near space segment accounted for the largest revenue share of around 40.5% in 2022. Near-space or orbital robots can be used for repairing satellites, assembling large space telescopes, and deploying assets in space for scientific exploration.

Solutions Insights

The Remotely Operated Vehicles (ROV) segment accounted for the largest revenue share of 37.6% in 2022 and is expected to expand at the fastest CAGR during the forecast period. The ROVs segment is further categorized into rovers/spacecraft landers, space probes, and others.

Regional Insights

North America dominated the space robotics industry and accounted for the largest revenue share of 55.0% in 2022. The regional market growth is attributed to the strong space capabilities of NASA and CSA. The regional market growth is attributed to the strong space capabilities of NASA and CSA. Both organizations invest huge amounts in R&D and technology enhancement to execute space exploration initiatives.

Organization Type Insights

The government segment held the largest revenue share of 69.5% in 2022. Several R&D activities and satellite launches for defense & and security purposes are escalating the demand for robotics technologies in this segment.

Key Space Robotics Companies:

ALTIUS SPACE MACHINES.

ASTROBOTIC TECHNOLOGY

BluHaptics, Inc.

Honeybee Robotics

Intuitive Machines, LLC.

MAXAR TECHNOLOGIES

Metecs, LLC.

Motiv Space Systems, Inc.

Northrop Grumman.

Oceaneering International, Inc.

Recent Developments

In March 2023, Honeybee Robotics, LLC, announced the opening of a new office in Greenbelt, Maryland. The facility focuses on engineering and program management, featuring state-of-the-art equipment for efficient hardware development.

In November 2022, NASA chose Honeybee Robotics to design, build, and deploy the Spin Eject Mechanics (SEM) on the Mars Sample Return Mission (MSR). During launch, cruise, and on-orbit operations around Mars, the SEM was planned to control the Earth Entry System (EES). However, SEM's primary duty is to release the EES from the MSR Earth Return Orbiter spacecraft.

In October 2021, the Japanese space robotics start-up GITAI declared that it carried out a technical demonstration of an autonomous space robot inside the ISS (International Space Station), performing various tasks. NASA plans to place the robot inside the NanoRacks Bishop Airlock at the ISS after a successful technical demonstration.

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Israel's International Trade: Important Suppliers, Leading Exporters, and the Effect of New Sanctions

Overview: Due to the Gaza War, the UK halts trade negotiations.

In reaction to Israel's military activities in Gaza and the growth of illegal settlements in the West Bank, the United Kingdom has suspended free trade talks with the country.

Foreign Secretary David Lammy's announcement of this action reflects mounting dissatisfaction with Israel's behavior around the world.

However, what is the size of Israel's international commerce and which nations are its main trading partners?

Important Trade Data (2024)

Imports in total: $91.5 billion

Exports in total: $61.7 billion

Deficit in Trade: $29.8 billion

Israel imports petroleum, automobiles, and machinery and exports primarily electronics, diamonds, and pharmaceuticals.

Leading Nations That Trade With Israel

Israel's Top Exports to the US: Diamonds, Electronics, and Pharmaceuticals ($17.3B)

Integrated circuits (Intel chips) in Ireland ($3.2B)

Hong Kong ($2B) + China ($2.8B) = $4.8B total - chemicals, optics

India ($2.5B): equipment and chemicals

Netherlands ($2.1B): Tech components and diamonds

Israel’s Top Import Sources

China ($19B) – EVs, phones, computers

United States ($9.4B) – Weapons, diamonds, tech

Germany ($5.6B) – Cars, pharmaceuticals

Switzerland ($4.8B) – Precision instruments, drugs

Italy ($3.9B) – Machinery, fashion goods

Why Did the UK Put a Stop to Trade Negotiations?

Since October 2023, more over 40,000 Palestinians have been murdered in the Gaza War.

Settlements on the West Bank: UK declares growth "illegal and destabilizing."

Current Trade: The UK exports $1.57 billion in diamonds and technology and imports $1.96 billion in jet engines and medications from Israel.

EU Examining Trade Partnerships A reevaluation of trade relations with Israel across the union was acknowledged by EU foreign policy leader Kaja Kallas.

What Are the Main Exports from Israel?

Electronics & Machinery ($18 billion): military technology, Intel processors

Teva generics in Chemicals & Pharmaceuticals ($10B)

Diamonds & Jewelry ($9B): The world's largest supplier of cut diamonds

Medical Equipment ($7B): Surgical instruments and imaging equipment

Oil & Minerals ($5B): Potash and refined petroleum

The Potential Economic Impact of Sanctions on Israel

Trade restrictions from the UK and EU could disrupt over $5 billion in annual trade.

Ireland, Intel's EU base, is a significant buyer, putting the tech sector at danger.

The diamond industry is susceptible to supply shifts from Belgium, India, and the UAE.

Questions and Answers (FAQs)

1. What makes Ireland one of Israel's top buyers? Ireland imports $3 billion worth of Israeli microchips, which are supplied to EU markets by Intel's Kiryat Gat plant.

2. Does Israel's military spending benefit the US? Yes, $3.8 billion in military aid is used annually to help pay for some of the US's weapons exports to Israel.

3. If sanctions increase, might trade with China supplant that with the West?

Partly—Israel still imports 20% of its goods from China, but it still depends heavily on the US and EU for technology.

4. What will happen to Israel's economy next? In the short term: minimal effect (US commerce remains robust).

Conclusion: A Changing Environment for Trade

Despite being vulnerable to Western sanctions, Israel's economy is nonetheless strong. The economic effects of the war are only getting started, as the UK has frozen trade discussions and the EU is reevaluating ties.

Will additional nations stop doing business with Israel? Stay tuned for further information as diplomatic demands mount.

0 notes

Text

Weill-Marchesani Syndrome Market Size, Share, Trends, Demand, Growth and Competitive Outlook

Global Weill-Marchesani Syndrome Market' - Size, Share, Demand, Industry Trends and Opportunities

Global Weill-Marchesani Syndrome Market, By Treatment (Medication, Laser Therapy, Surgery, Genetic Counseling, Others), Diagnosis (Tonometry, Visual Field Testing, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Genetic Testing, Others), Symptoms (Glaucoma, Brachydactyly, Microspherophakia, Joint Stiffness, Myopia, Short Stature, Others), Demographic (Infancy, Neonatal), Dosage (Tablet, Injection, Others), Route of Administration (Oral, Intravenous, Others), End-Users (Clinic, Hospital, Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy), Country (U.S., Canada, Mexico, Brazil, Argentina, Peru, Rest of South America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Hungary, Lithuania, Austria, Ireland, Norway, Poland, Rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Vietnam, Rest of Asia-Pacific, Saudi Arabia, U.A.E, Egypt, Israel, Kuwait, South Africa, Rest of Middle East and Africa) Industry Trends

Access Full 350 Pages PDF Report @

**Segments**

- **Cause of Weill-Marchesani Syndrome**: One of the key segments in the market analysis of Weill-Marchesani Syndrome is the cause of the condition. This genetic disorder is primarily caused by mutations in the ADAMTS10 and FBN1 genes. Understanding the genetic basis of Weill-Marchesani Syndrome is crucial for developing targeted therapies and diagnostic tools for this rare disorder.

- **Symptoms and Diagnosis**: Another important segment is the symptoms and diagnosis of Weill-Marchesani Syndrome. Patients with this condition often present with short stature, microspherophakia, and joint stiffness. Diagnosis involves a thorough clinical examination, genetic testing, and imaging studies to assess the severity of the disease and its impact on various organ systems.

- **Treatment and Management**: The treatment and management segment of the Weill-Marchesani Syndrome market focuses on the current therapies available for patients with this condition. Management typically involves a multidisciplinary approach, including surgical interventions to address ocular complications and physical therapy to manage joint stiffness. Developing novel treatment options for Weill-Marchesani Syndrome remains a significant unmet need in the market.

**Market Players**

- **BioMarin Pharmaceutical Inc.**: BioMarin is a key player in the rare disease space and has been involved in the development of therapies for genetic disorders such as Weill-Marchesani Syndrome. The company's research and development efforts in the field of gene therapy and precision medicine could have a significant impact on the treatment landscape for this condition.

- **Regeneron Pharmaceuticals Inc.**: Regeneron is another market player that has shown interest in rare genetic disorders like Weill-Marchesani Syndrome. The company's focus on genetic engineering and innovative treatment modalities positions them as a potential leader in developing targeted therapies for this rare condition.

- **Spark Therapeutics**: Spark Therapeutics is known for its expertise in gene therapy, which could be a promising approach for treatingBioMarin Pharmaceutical Inc., Regeneron Pharmaceuticals Inc., and Spark Therapeutics are significant players in the market analysis of Weill-Marchesani Syndrome. These companies are actively involved in research and development efforts to address the unmet needs in treating this rare genetic disorder. With a focus on gene therapy and precision medicine, these market players are at the forefront of developing innovative therapies for Weill-Marchesani Syndrome. BioMarin's established presence in the rare disease space gives them a competitive advantage in leveraging their expertise to create targeted treatments for genetic disorders like Weill-Marchesani Syndrome. Regeneron's commitment to genetic engineering and cutting-edge treatment modalities positions them as a potential leader in advancing therapies specifically tailored for this condition. Spark Therapeutics, known for its proficiency in gene therapy, brings a unique perspective to the market analysis of Weill-Marchesani Syndrome by exploring novel approaches to address the underlying genetic mutations driving the disease.

In the cause segment of Weill-Marchesani Syndrome market analysis, an in-depth understanding of the genetic basis of this condition is paramount. Mutations in the ADAMTS10 and FBN1 genes have been identified as the primary causes of Weill-Marchesani Syndrome. This genetic insight is crucial for developing targeted therapies that address the underlying mechanisms of the disorder, paving the way for more effective treatment strategies. By unraveling the genetic intricacies of Weill-Marchesani Syndrome, market players can tailor their research and development efforts towards precision medicine approaches that aim to correct the genetic anomalies responsible for the disease.

The symptoms and diagnosis segment of the market analysis for Weill-Marchesani Syndrome sheds light on the clinical presentation and diagnostic methods used to identify and evaluate patients with this rare genetic disorder. Patients with Weill-Marchesani Syndrome often exhibit distinct symptoms such as short stature, microspherophakia, and joint stiffness, which require a comprehensive clinical assessment for accurate diagnosis. Through genetic testing and imaging**Global Weill-Marchesani Syndrome Market Analysis:**

- **Treatment:** The market for Weill-Marchesani Syndrome treatment includes medication, laser therapy, surgery, genetic counseling, and other therapeutic interventions. The development of novel treatment options, particularly in gene therapy and precision medicine, remains a crucial area of focus for market players to address the unmet medical needs in managing this rare genetic disorder.

- **Diagnosis:** Diagnosis of Weill-Marchesani Syndrome involves various methodologies such as tonometry, visual field testing, computed tomography (CT), magnetic resonance imaging (MRI), genetic testing, and other diagnostic tools. Accurate and timely diagnosis is essential for appropriate disease management and personalized treatment strategies tailored to the individual patient's needs.

- **Symptoms:** The symptoms of Weill-Marchesani Syndrome encompass a range of clinical manifestations including glaucoma, brachydactyly, microspherophakia, joint stiffness, myopia, short stature, and other associated symptoms. Understanding the diverse symptomatology of the condition is critical for early detection, intervention, and monitoring of disease progression.

- **Demographic:** Weill-Marchesani Syndrome can affect individuals across different age groups, with specific considerations for infants and neonates presenting unique challenges in diagnosis and management. The demographic profile of patients with this rare genetic disorder plays a significant role in shaping treatment strategies and healthcare delivery for optimal patient outcomes.

- **Dosage:** Treatment modalities for Weill

Key points covered in the report: -

The pivotal aspect considered in the global Weill-Marchesani Syndrome Market report consists of the major competitors functioning in the global market.

The report includes profiles of companies with prominent positions in the global market.

The sales, corporate strategies and technical capabilities of key manufacturers are also mentioned in the report.

The driving factors for the growth of the global Weill-Marchesani Syndrome Market are thoroughly explained along with in-depth descriptions of the industry end users.

The report also elucidates important application segments of the global market to readers/users.

This report performs a SWOT analysis of the market. In the final section, the report recalls the sentiments and perspectives of industry-prepared and trained experts.

The experts also evaluate the export/import policies that might propel the growth of the Global Weill-Marchesani Syndrome Market.

The Global Weill-Marchesani Syndrome Market report provides valuable information for policymakers, investors, stakeholders, service providers, producers, suppliers, and organizations operating in the industry and looking to purchase this research document.

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Global Weill-Marchesani Syndrome Market Landscape

Part 04: Global Weill-Marchesani Syndrome Market Sizing

Part 05: Global Weill-Marchesani Syndrome Market Segmentation by Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

The investment made in the study would provide you access to information such as:

Weill-Marchesani Syndrome Market [Global – Broken-down into regions]

Regional level split [North America, Europe, Asia Pacific, South America, Middle East & Africa]

Country-wise Market Size Split [of important countries with major market share]

Market Share and Revenue/Sales by leading players

Market Trends – Emerging Technologies/products/start-ups, PESTEL Analysis, SWOT Analysis, Porter’s Five Forces, etc.

Market Size

Market Size by application/industry verticals

Market Projections/Forecast

Browse Trending Reports:

Medical Waste Disposal Services Market Sexual Wellness Market Organic Poultry Feed Market Cloud Backup Market Seed Coating Colorants Market Immunoprotein Diagnostic Testing Market Wavefront Aberrometer Market Phenol Market Smart Toys Market Stand-Up Paddleboard Market Blockchain Insuretech Market Omega-6 Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]

0 notes

Text

Application Transformation Market: Can Enterprises Fully Modernize by 2032

The Application Transformation Market was valued at USD 11.56 billion in 2023 and is expected to reach USD 42.40 billion by 2032, growing at a CAGR of 15.58% from 2024-2032.

Application Transformation Market is witnessing rapid evolution as enterprises modernize legacy systems to adapt to digital-first strategies. With the growing need for agility, scalability, and cloud-native architectures, companies across industries are reengineering core applications to align with today’s dynamic business environments.

U.S. enterprises are leading the charge in adopting advanced transformation frameworks to unlock operational efficiency and competitive advantage.

Application Transformation Market continues to expand as organizations prioritize innovation and resilience. Modernization initiatives are being accelerated by cloud migration, DevOps adoption, and increased pressure to reduce technical debt and improve time-to-market.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6639

Market Keyplayers:

Accenture (myNav, CloudWorks)

Atos SE (Atos CloudCatalyst, Atos Codex)

BELL-INTEGRATION.COM (Cloud Migration Services, Workload Transformation)

Capgemini (Perform AI, Cloud Platform Engineering)

Cognizant (Cloud360, Modern Application Services)

Fujitsu (Modernization Assessment, RunMyProcess)

HCL Technologies Limited (Cloud Native Lab, Application 360)

International Business Machines Corporation (Cloud Pak for Applications, IBM Mono2Micro)

Infosys Limited (Infosys Cobalt, Live Enterprise Application Development Platform)

Microsoft (Azure Migrate, Visual Studio App Center)

Open Text (OpenText Cloud Editions, AppWorks)

Oracle (Oracle Cloud Infrastructure, Oracle Application Express)

Trianz (CloudEndure, Concierto.Cloud)

Tech Mahindra (MoboApps, Application Lifecycle Management)

Pivotal Software (Pivotal Cloud Foundry, Spring Boot)

TCS (MasterCraft TransformPlus, Jile)

Asysco (AMT Framework, AMT Go)

Unisys (CloudForte, Unisys Stealth)

Hexaware (Amaze, Mobiquity)

Micro Focus (Enterprise Analyzer, Enterprise Server)

Market Analysis

The Application Transformation Market is being driven by the convergence of cloud computing, AI, and containerization technologies. Businesses in the U.S. and Europe are under mounting pressure to streamline legacy infrastructure to enhance productivity and customer engagement. As digital transformation becomes central to business continuity, enterprises are investing in scalable, secure, and automated transformation services.

Companies are increasingly moving away from monolithic applications toward microservices-based architectures. This transition allows for rapid development, lower maintenance costs, and seamless integration with modern tech stacks. Regulatory compliance, data sovereignty, and the need to deliver faster services are also contributing to the market’s momentum.

Market Trends

Shift toward cloud-native and serverless computing environments

Adoption of DevOps and CI/CD for streamlined deployment

Rise in demand for container orchestration tools like Kubernetes

Integration of AI/ML to enhance application efficiency and analytics

Increased focus on legacy system replatforming and refactoring

Use of low-code/no-code platforms for faster modernization

Growing reliance on third-party managed service providers

Market Scope

The scope of the Application Transformation Market spans industries from healthcare to finance, where mission-critical systems are being reengineered to meet digital demands. Businesses now view transformation not just as a technology upgrade but a strategic imperative.

Legacy application modernization to reduce technical debt

Enterprise cloud migration and hybrid deployment strategies

API enablement for improved integration across platforms

Enhanced security and compliance through modernization

Seamless user experience via responsive and modular designs

Scalable infrastructures designed for future-ready operations

Forecast Outlook

The Application Transformation Market is positioned for sustained growth as digital-first operations become a top priority for global businesses. With advancements in cloud ecosystems, automation frameworks, and development methodologies, the transformation journey is becoming more agile and efficient. U.S. and European markets will remain key innovation hubs, driven by enterprise cloud adoption, skilled IT ecosystems, and regulatory frameworks that promote modernization. Organizations that embrace early transformation strategies will gain a long-term edge in operational efficiency, cost savings, and customer satisfaction.

Access Complete Report: https://www.snsinsider.com/reports/application-transformation-market-6639

Conclusion

The Application Transformation Market is reshaping the digital landscape by converting outdated systems into smart, scalable platforms that support long-term innovation. Enterprises aiming for future readiness are leveraging this transformation to stay ahead in a competitive and rapidly changing environment. Whether in New York or Frankfurt, modernized applications are becoming the backbone of resilient and responsive businesses—making transformation not a trend, but a business necessity.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.